Managing risks in project management is the most challenging piece of a complex puzzle. Without risk management, cost, resource allocation, environmental factors, and time constraints can all endanger a project's success.

In this article, we'll review the basics of project management and the three different types of risk you may face. Then we'll explore how to address (or avoid) project risks. In doing so, we'll give you all the tools you need to start your next project without worrying.

Once you've learned the ins and outs of project risk management, you can apply these to any size project in the future.

What is project risk management?

Project risk management is a crucial activity in project management. Risks that occur during a project can be extremely costly and time-consuming. Potential risks can also throw your project over budget or make it impossible to meet deadlines if they come to fruition. Identifying, understanding, and mitigating risks can help your project run smoothly without any emergent costs or delays. Ignoring project risks can derail a project quickly.

A risk management strategy helps you consider all known risks and have a plan in place should they arise. This process does require time (and, sometimes, financial investment). However, investing these resources before a project begins can ensure a project's success and that all key performance indicators (KPIs) are met along the way.

Let's look at a small business pet store owned by Molly. Molly wants to build a section where pet owners can groom their pets in stores. Molly needs to determine first what her goals are. For example, goals could include increasing profits, gaining additional customers, or upselling existing customers.

Three types of project management risk

There are three primary types of project risks: schedule risk, performance risk, and cost risk.

|

Schedule Risk

Schedule risk is the likelihood of not meeting predetermined deadlines. There are lots of factors that can cause schedule risk. Some examples of these are delays in deliveries of materials, longer (than anticipated) hiring timelines, travel delays, and scope creep.

While not all of these risks can be avoided, some, such as scope creep, can. Scope creep, which happens when a project becomes larger than expected, can eat up finite resources and delay the project’s timeline.

Molly would like to complete her project in six months. Finding a labor force available within this time frame is an example of schedule risk.

Performance Risk

Performance risk is the likelihood the project won't produce the planned project goals. Unmitigated or predicted performance risk can halt a project in its tracks.

Examples of performance risk include volatility in labor, material cost, or delivery timelines. When examining performance risk, it's essential to consider that the potential outcomes aren't success or failure. Outcomes may vary based on cost, time, and production level. As with all types of risk, understanding performance risk is key to making sure a project succeeds.

Molly also faces performance risk. She may do everything within her power to complete the project on time, but still not see the results she wants in her profits.

Cost risk

Cost risk in project management is the one risk that's most anticipated. Small businesses run on small margins, and additional costs without a contingency budget can have severe consequences. The stakes are high for small businesses when it comes to cost risk.

Some common risk factors that cause project cost risks are unanticipated labor, permit, legal, administrative, or material costs. If these aren't managed from the get-go, the project budget will be in danger.

Small businesses like Molly’s need to pay close attention to cost risk. In Molly’s project, the cost of installation, materials, and labor can all have a direct impact on the project’s success.

Positive risk

A lesser-known risk in project risk management is positive risk. Positive risk occurs when something positively impacts the project's outcome.

|

Positive risks include new technology that can speed up a project timeline, efficiencies that'll reduce cost, or policy changes. While positive risk is a good thing, you should still try to identify it proactively and develop a plan to take advantage of it should it occur.

In Molly’s case, an example of positive risk could be that a local supply company is going out of business and offering plumbing supplies at a deeply discounted rate, thus lowering her cost of materials.

The 5 steps of project risk management

Many small businesses assume they're too small for a risk management process. However, a risk that happens to a small business may have a much more significant impact than the same risk would have on a large corporation.

For example, a government fine levied against a large company might be the cost of doing business. The same fine imposed against a small business might represent their marketing budget for the coming year.

Addressing risks head-on will help you avoid or lessen the potential negative outcome of those risks.

That said, there are five basic steps you can take to project risk management mitigation.

1. Identify potential project risks

The first step to making sure risks don't endanger your project is identifying them. This may sound simple. However, it's critical to spend some time investigating potential risks. Investigating risks is accomplished through brainstorming sessions, interviewing team members, and investigating costs. Complete all of these tasks before the project begins.

Once you have identified the potential risks, you'll want to do a risk analysis, which can take many forms.

2. Gauge risk probability (and potential impact)

In this step of your risk assessment, you'll want to determine the probability of the risk occurring (also known as the risk probability). Risks with a low probability of occurrence don't need dedicated resources as imminently as risks that are very likely to happen.

You'll also want to determine the impact of the risks should they occur. If a risk's occurrence would endanger the project's completion, that risk needs attention immediately. If another risk would delay the project's timeline by a few days, that risk is less important to address.

3. Prioritize risks

Once risks are identified and their likelihood (and impact) determined, the next step is to prioritize them. Give the highest priority to the risks that are likely to occur or would tank the project. Risks usually fall into one of five categories:

- Tolerable risk: A risk of little or no concern.

- Low risk: A risk of very minimal impact.

- Medium risk: A risk that’d impact the project's cost, timeline, or goals.

- High risk: A risk with an increased likelihood of occurrence and would significantly impact the project outcome.

- Intolerable risk: A risk that, if it occurred, would cause the project to fail.

You can use a risk matrix template to visualize this. A project risk matrix, or a project risk register, allows businesses to determine the most pressing risks. A risk register is a primary project risk reporting tool.

4. Assign ownership of the risks

Once you have placed each risk into a (prioritized) category, it's time to assign each to a person. Although this step is optional, having risk owners is highly recommended as it will increase accountability. The person assigned to the risk is tasked with tracking and mitigating the risk.

5. Continuously track risks

Keeping a watchful eye on known risks or watching for new risks is an ongoing affair.

For example, if you are building a warehouse, the cost of materials may fluctuate daily. These cost variances need assessment to determine the proper time to purchase the necessary supplies. And you'll also want to watch for new risks not previously identified.

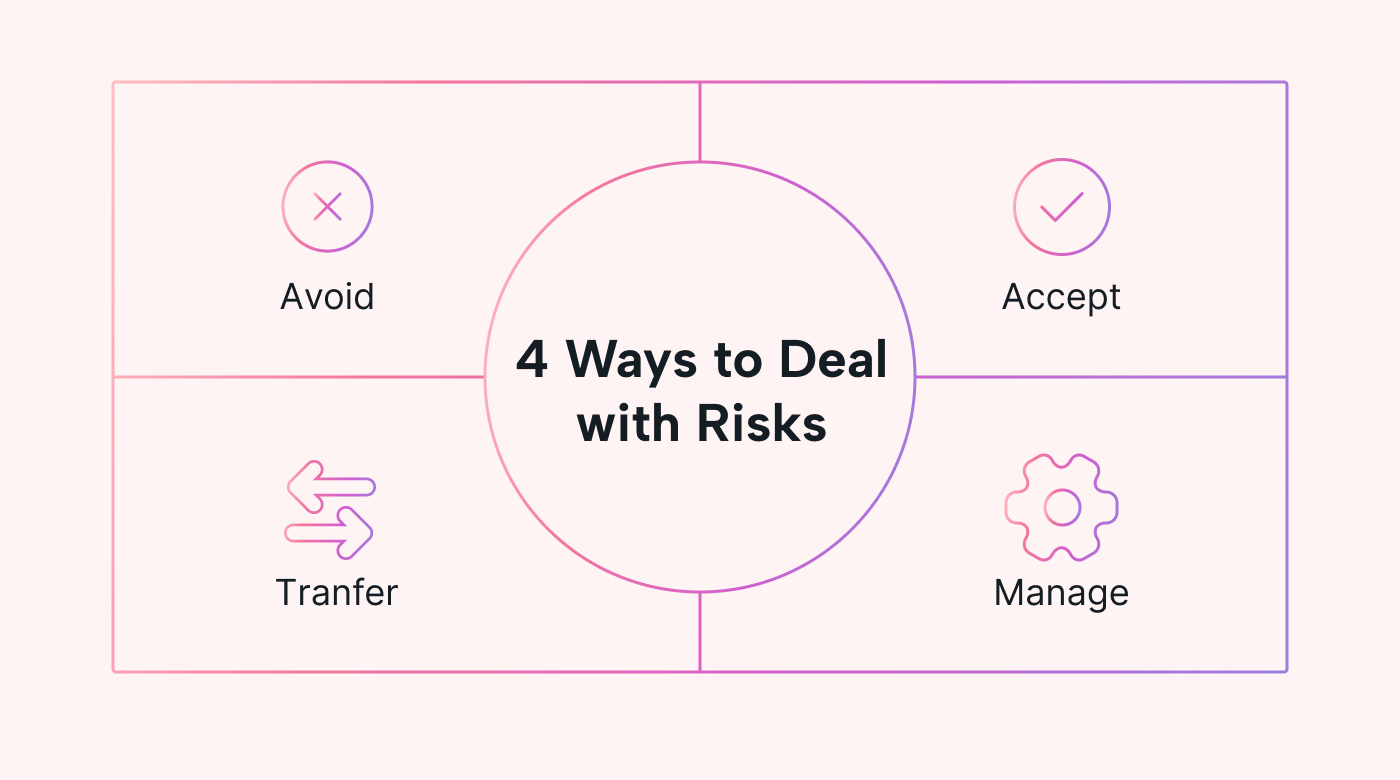

Four ways to deal with risk

There are four ways to deal with risks. Even positive risks need contingency plans so you can take advantage of them.

|

Avoid risk

While you can't avoid all risks, you can sidestep some risks.

For example, if the price of a material in a product fluctuates wildly, you can try to find new material with stable prices. Substituting that material would allow you to avoid this risk.

Accept the risk

The second option for risk management is accepting and addressing the risk. If the risk potential is high, addressing it at the start of the project will help you minimize its impact.

You'll probably have to allocate money, resources, and/or time to accept (and manage) risks.

Transfer the Risk

Transferring risks is another way to mitigate identified risks.

For example, you can purchase insurance to transfer the risks from the business to an insurance company. Risk transfer is an effective and safe risk mitigation technique, but can be costly.

Manage the risk

Managing (or minimizing) the risk is another way for a small business to ensure the project succeeds.

Minimizing risk can come in many forms, such as risk monitoring and control. The Project Management Institute also provides checklists and suggestions for mitigating risk.

Common pitfalls in project risk management

You should look out for some common pitfalls when assessing and managing project risks.

At the top of the list is taking shortcuts when planning a project.

When small business resources are limited, taking shortcuts in planning is easy. However, thinking through a project from a 10,000-foot view will allow you to see the risks associated with the project.

|

Some other common pitfalls are unrealistic targets, poor communication, unclear job roles, and a lack of alternative plans. Effective communication makes it easier for everyone to work together to remove risks.

Clear communication can also prevent miscommunication of responsibilities. Often, unrealistic targets and, thus, risks arise from failing to ask the right people the right questions.

One of the actions Molly can take to mitigate risks is to thoroughly research predicted costs of materials and labor ahead of time. Obtaining permit costs and timelines is another critical project management piece for Molly. If she has employees, discussing the project with them, getting their input, and brainstorming will make the process go more smoothly.

Using project management tools for project risk management

Managing potential project risks is a critical element of project management. It requires time and resources to anticipate and understand risks. The investment of time and resources at the beginning of a project can save you a great deal of time and money.

Project management tools can help you significantly decrease the likelihood of risks derailing your projects. They're great for facilitating communication and visualizing projects.

For example, a time-tracking tool will enable you to determine what project pieces require the most work. Motion's time-tracking tool is an easy-to-implement option that allows you to see the allocation of resources.

|

Putting all your project management documentation into a single place guarantees that the information is current. This way, no one makes decisions based on outdated information.

Many projects include stakeholders (and customers) spread out geographically. Project management software will help with communication. Everyone should be able to access the project's status and tasks from their mobile devices.

Control your project risk management with Motion

Project risk management isn't the most glamorous part of managing a project. However, by addressing risks right from the beginning of a project and having a risk response plan, you can ensure that nothing lurks in the shadows that'll surprise you when you least expect it.

Motion's easy-to-learn (and implement) functionality can help implement your risk management plan (and see what everyone is doing at all times).

For example, Motion can digitize all of those whiteboards and post-it notes. You don't need to remember what risk mitigation plan you developed in the meeting three weeks ago because it'll be in Motion.

Motion also allows you to easily assign tasks and see the project from a birds-eye view, all from your computer or phone.